This is a market that simply refuses to break.

By most traditional measures, the headwinds are real. Mortgage rates remain elevated. Consumer confidence has been uneven. The federal workforce, always a key driver in this region, has faced its share of challenges. In fact, The DC metro lost 100,000 jobs in 2025 (-3.1%), the steepest decline among major metro areas, driven by federal

downsizing. And yet, here we are: prices largely stable, demand intact, and homes still trading hands at a steady (if unspectacular) pace.

The recent data drives this home.

In Northern Virginia, new contract activity rose nearly 12% year-over-year, with sales also up and median prices climbing 4.5%, all while months of supply held at just 1.2 months. That’s not a market under stress; that’s a market doing push-ups.

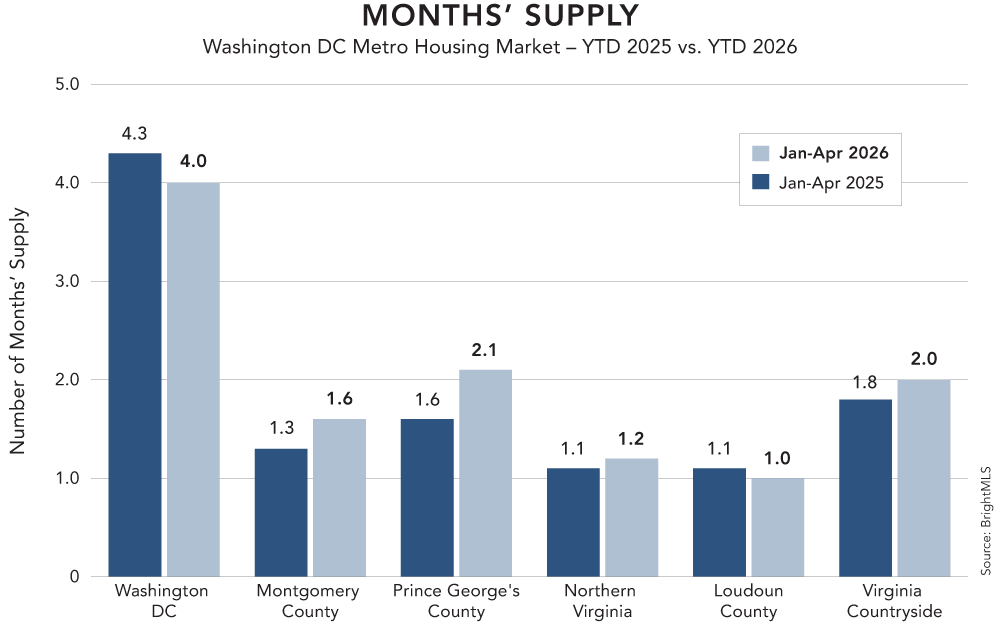

Even in Washington, DC, which has been the softest part of the region, new contracts were up 8.7%, and months’ supply declined from 4.6 to 3.9. Yes, prices were down year-over-year, and days on market stretched a bit, but demand is quietly improving beneath the surface.

Meanwhile, Montgomery and Prince George’s Counties, Maryland, tell a more nuanced story. Inventory is rising, up nearly 20% and 34%, respectively, and days on market have increased meaningfully. And yet, contract activity is still up in both jurisdictions. Buyers haven’t disappeared; they’ve just become more selective and they are in no particular hurry.

Loudoun County posted steady gains in both sales and contracts, has the lowest supply in the region at just 1.1 months, and actually has 6% less inventory. The Virginia Countryside saw prices rise nearly 7% with improving urgency. Not exactly signs of a market waving a white flag.

So what’s going on?

The underlying story hasn’t changed. The DC region continues to benefit from a highly educated, high-income workforce and a structural shortage of housing that didn’t magically resolve itself when rates went up. Those fundamentals are doing a lot of heavy lifting.

What has changed is behavior.

Buyers are more deliberate. Sellers are more strategic. The margin for error, especially on pricing, has narrowed considerably. In some areas, that means longer market times and more negotiation. In others, it still means multiple offers and quick decisions. Same region, different realities.

In many ways, this is a healthier version of the market. Less adrenaline, more discipline. Fewer bidding wars, more thoughtful decisions.

So no, the market hasn’t broken. It’s adapted.

And if anything, recent numbers suggest it’s getting pretty good at it.

PARTNERED AFFILIATES

Copyright © Corcoran 2023 – 2026. Corcoran and the Corcoran Logo are trademarks of Corcoran Group LLC. Corcoran Group LLC fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each office is independently owned and operated. Any services or products provided by independently owned and operated offices are not provided by, affiliated with, or related to Corcoran Group LLC nor any of its affiliated companies.

© Corcoran McEnearney 2026. All rights reserved. DO NOT SELL MY PERSONAL INFORMATION

Peter Pejacsevich, VA Broker | David Howell, MD & DC Broker | Josh Beall, WV Broker

PARTNERED AFFILIATES

Copyright © Corcoran 2023 – 2026. Corcoran and the Corcoran Logo are trademarks of Corcoran Group LLC. Corcoran Group LLC fully supports the principles of the Fair Housing Act and the Equal Opportunity Act. Each office is independently owned and operated. Any services or products provided by independently owned and operated offices are not provided by, affiliated with, or related to Corcoran Group LLC nor any of its affiliated companies.

© Corcoran McEnearney 2026. All rights reserved.

DO NOT SELL MY PERSONAL INFORMATION

Peter Pejacsevich, VA Broker | David Howell, MD & DC Broker | Josh Beall, WV Broker